Some colleges use financial aid for many more purposes than helping poor students attend.Glen Cooper/Getty Images

DON'T MISS STORIES.FOLLOW VOX!

Most financial aid isn't really about helping students pay for college.

Instead, it's part of an elaborate strategy colleges use to attract the students they want, admit the students they need and encourage others to stay away.

Federal grants overwhelmingly go to poor students. But scholarships and grants offered by colleges themselves — which account for 19 percent of all financial aid—are all over the map. Private colleges pioneered grants and financial aid offers to boost rankings and attract the wealthy, but in an era of shrinking state budgets, public colleges are increasingly likely to play the same game. And that's only the beginning of what colleges don't mention about financial aid.

Whether you need financial aid could affect whether you get into college

George Washington University made headlines this year for lying about its need-aware admissions policies.Astrid Riecken/The Washington Post/Getty Images

This is especially true for students who are teetering on the edge of admission, who end up on a wait list, or who are trying to transfer. Admitting students without considering whether they can pay is considered the gold standard of college admissions. It's how things work for in-state students at public colleges, which tend to have lower tuition. But at private colleges, it's rare, and getting rarer: Of the 1,600 private nonprofit colleges in the U.S., few admit students without considering family income at all.

Transfer students, wait-listed students and international students are the most likely to have financial need considered at some point. This happens even at selective, wealthy universities with huge endowments. Brown University and Vanderbilt University, to name two, both consider transfer students' financial need in admissions decisions.

It might be common, but that doesn't mean it's popular. When George Washington University said last year it had lied about taking students' need into account in admissions, it caused an uproar.

Admissions officers say financial need is rarely the determining factor and is most likely to affect students who would just barely make it in otherwise. (At George Washington, admissions officers said only a few borderline students will be affected this year.)

A college that promises to meet a student's financial needs isn't promising a debt-free education

Instead, they're promising a financial aid "package" — including grants, which don't have to be paid back, and loans, which do — that covers the difference between the price of tuition and the family's expected contribution. Even if colleges meet their full need, students whose parents are paying for college could still be required to borrow up to $31,000 in federal loans over the course of a four-year degree.

Federal loans do have to be paid back, with interest. But they're considered financial aid because they're handed out without a credit check and at lower rates than students would pay a bank or credit-card company.

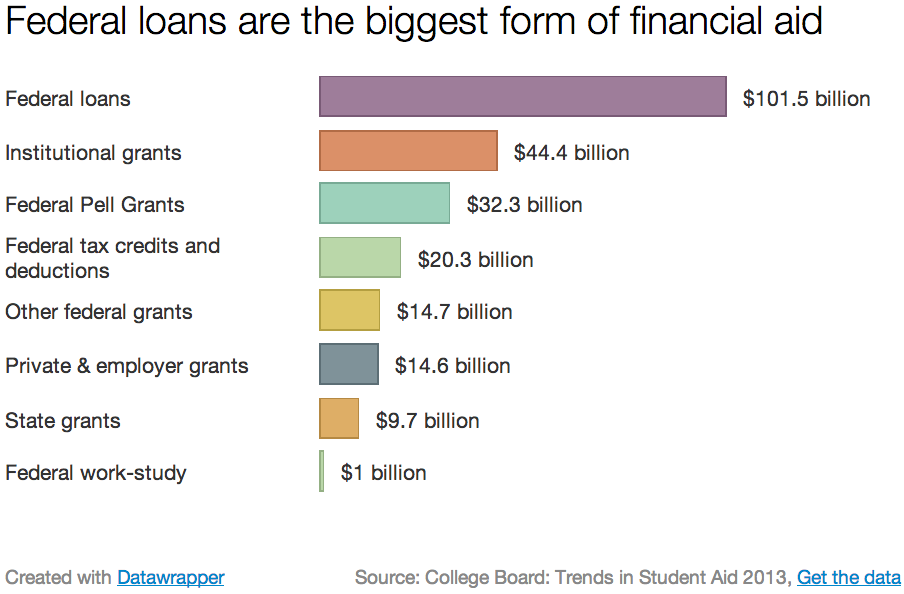

Federal loans are the largest share of financial aid: $101.5 billion annually, dwarfing the $32.3 billion in federal Pell grants, $44.4 billion in colleges' own grants and scholarships, and $9.7 billion in state grants handed out each year.

Many colleges, though, don't promise to meet a student's full financial need. Like admitting students without regard to their financial situation, it's a promise many can't afford to make. Students at those colleges are likely to have to borrow even more. .

‘Merit' aid isn't just for the smart kids

Say a college has $30,000 to give away in financial aid. It can either use that money cover the full price for one low-income student, or flatter five with $6,000 "scholarships" who can pay the rest themselves. The latter is much better for the college's bottom line.

That's a big, unspoken role for aid not based on financial needs: enticing students to attend one college rather than another. Sometimes those awards are true scholarships, given to students with impressive achievements or who have high grades and test scores that will help a college raise its academic profile and climb in the influential U.S. News & World Report rankings.

The University of Rochester was unusually candid in a 2011 blog post on the factors that go into its merit aid program. The biggest bonus was, essentially, for just showing up: Students who had "serious" conversations and filled out all their financial aid paperwork received thousands of dollars more.

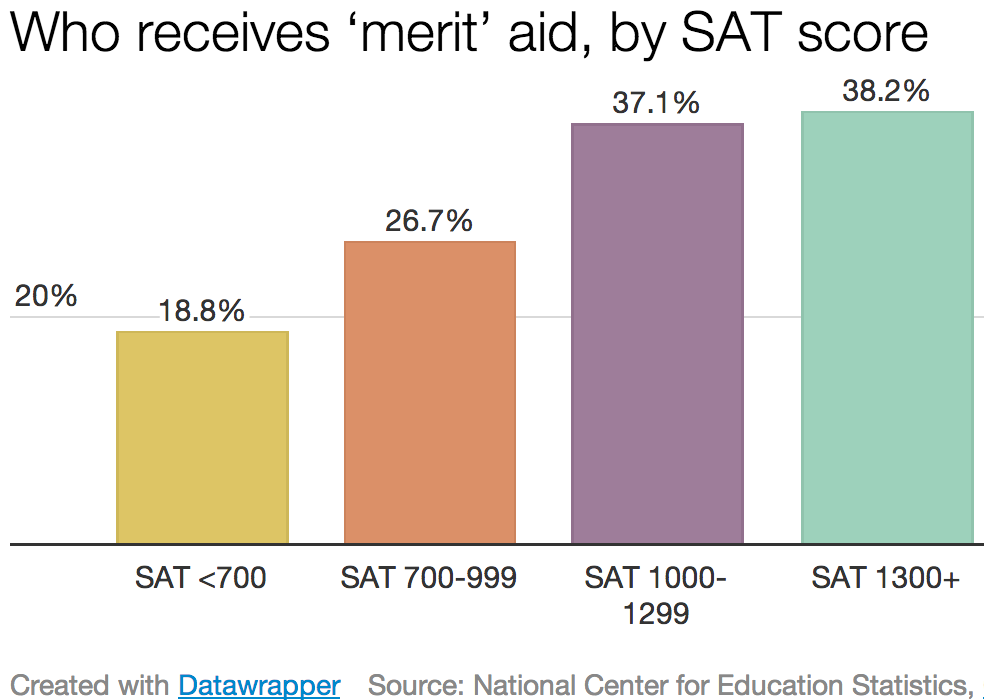

Some recipients of merit aid are below average academically. One in 5 college students with combined SAT scores below 700 — out of a possible 1600 — received "merit" aid in 2007, according to the National Center for Education Statistics. So did more than one-quarter of students with SAT scores below 1000. And so did one in five students with below a C average in college.

Some of those awards might recognize talents in areas other than academics (athletic scholarships, for example, often go to athletes with relatively low SAT scores). But many are small scholarships meant to attract students who can afford to pay the rest, writes the New America Foundation's Stephen Burd, who has studied the growth of merit aid at the expense of need-based aid.

"In a lot of cases, they are trying to get full-pay students," Burd said, calling the practice "affirmative action for the rich."

The goal of a financial aid package might be to persuade you not to come

John Greim/LightRocket via Getty Images

In the world of college admissions and aid, this is called an "admit-deny," an enrollment manager told The Atlantic in 2005: Let a student in, but offer a financial aid package so meager they'd be crazy to accept it. Colleges can leave a wide gulf between financial aid offers and the price of tuition — far too wide to be filled with federal loans alone.

Admitting students without offering them enough aid to meet their need is common: 55 percent of all colleges, and 65 percent of private colleges, said they do so, according to a survey of admissions directors. (Two-thirds said they thought it was an ethical practice.)

In some cases, colleges expect families to take out additional private loans. In other cases, they expect that the poor financial aid package will dissuade them from coming at all. The problem is that not all families get the message, and end up taking on tens of thousands of dollars of debt each year.

The federal government helps high-earning families pay for college too.

But don't look for it on a financial aid award letter. Pell Grants go overwhelmingly to poor students: Most recipients come from families making less than $40,000 per year. That's led to criticism that the government doesn't do enough to help middle-income families, who are also worried about affording college.

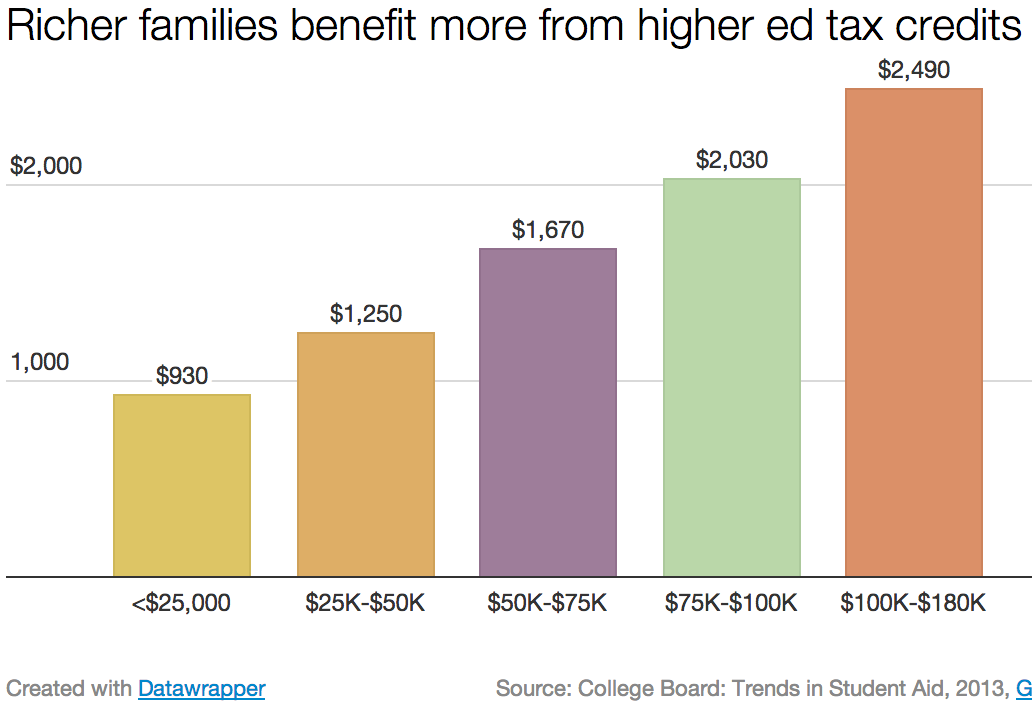

Middle-class and wealthy families, though, benefit from tax credits and deductions for tuition payments and student loan interest. (There's also a tax advantage for college savings.) Total tax credits and deductions for higher education expenses will add up to about $34 billion this year — slightly larger than the Pell Grant program. There is some overlap between the two programs: Some students receive both Pell Grants and tax credits, particularly the American Opportunity Tax Credit, which is refundable.

The average benefit from tax credits is smaller than the average Pell Grant: about $1,330 per recipient, compared with more than $3,000 per recipient on average for a Pell Grant. But wealthier families benefit more. Families making between $100,000 and $180,000 get the most annually, an average of almost $2,500 in tax benefits, according to the College Board.

How much you take out in loans might not be how much you pay back.

Citing bank bailouts, student protesters call for student debt cancelations. The Education Department does forgive some loans through income-based repayment. David McNew/Getty Images

Here's a form of after-the-fact financial aid that doesn't show up before students enroll. The Education Department's income-based student loan repayment programs remain something of a well-kept secret despite an intense outreach campaign.

Those programs, which are available only for federal student loans, base monthly payments on borrowers' incomes. Borrowers pay for up to 20 years (10 if they work at a nonprofit or government agency). Either they pay back the amount they borrowed plus interest, or the remaining balance is forgiven.

That means if borrowers take on a lot of debt, then can't find a job or go into a low-paying career, their monthly payments are lower than they'd be under a standard repayment plan. If they're doing well, they pay off their loans quickly. (There's no risk that they will pay back more than they owe.) If they continue to struggle, the loans will eventually be forgiven.

There are two general types of loans: federal loans and private loans. Federal loans are issued by the Education Department. Private loans come from banks. Federal loans have some protection that private loans don't, including more flexible repayment options and the possibility of eventual loan forgiveness. Neither kind is dischargeable in bankruptcy.

The Education Department makes the vast majority of student loans itself, directly to students, so they're called direct loans. Since 2013, interest rates have been based on the 10-year Treasury bond rate, so they fluctuate from year to year.

Students are limited in how much they can borrow in federal loans. Dependent students can borrow no more than $31,000 during their college careers in direct loans, and no more than $23,000 of that amount can be subsidized. Independent students are limited to $57,500 total.

Direct Subsidized Loans for undergraduates. These loans are offered based on financial need and don't accumulate interest while the borrower is enrolled in college. Interest rate for 2013-14: 3.86 percent.

Direct Unsubsidized Loans for undergraduates. These loans are available to undergraduates regardless of financial need, but interest accumulates while borrowers are in college, making the loan more expensive in the long run. Most subsidized loan borrowers also have unsubsidized loans. Interest rate for 2013-14: 3.86 percent.

Direct Unsubsidized Loans for graduate students. Same deal as for undergrads, but at a higher interest rate. For 2013-14: 5.41 percent. Graduate students can borrow up to $20,500 per year.

Direct PLUS loans. Graduate students and parents of undergraduate students can borrow up to the cost of attendance, which includes living expenses, at a higher interest rate. For 2013-14: 6.41 percent.

Perkins loans. These loans for undergraduates are based on financial need and are administered by colleges. Interest doesn't accumulate while borrowers are in school. Interest rate for 2013-14: 5 percent.

The problem, of course, is that these people are also affecting, and in some cases controlling, the levers of government. And this, Kahan says, is where identity-protective cognition gets dangerous. What’s sensible for individuals can be deadly for groups. "Although it is effectively costless for any individual to form a perception of climate-change risk that is wrong but culturally congenial, it is very harmful to collective welfare for individuals in aggregate to form beliefs this way," Kahan writes. The ice caps don’t care if it’s rational for us to worry about our friendships. If the world keeps warming, they’re going to melt regardless of how good our individual reasons for doing nothing are."

To spend much time with Kahan’s research is to stare into a kind of intellectual abyss. If the work of gathering evidence and reasoning through thorny, polarizing political questions is actually the process by which we trick ourselves into finding the answers we want, then what’s the right way to search for answers? How can we know the answers we come up with, no matter how well-intentioned, aren’t just more motivated cognition? How can we know the experts we’re relying on haven’t subtly biased their answers, too? How can I know that this article isn’t a form of identity protection? Kahan’s research tells us we can’t trust our own reason. How do we reason our way out of that?

Instead, they're promising a financial aid "package" — including grants, which don't have to be paid back, and loans, which do — that covers the difference between the price of tuition and the family's expected contribution. Even if colleges meet their full need, students whose parents are paying for college could still be required to borrow up to $31,000 in federal loans over the course of a four-year degree.

Instead, they're promising a financial aid "package" — including grants, which don't have to be paid back, and loans, which do — that covers the difference between the price of tuition and the family's expected contribution. Even if colleges meet their full need, students whose parents are paying for college could still be required to borrow up to $31,000 in federal loans over the course of a four-year degree.